December 4, 2025 | Mark Luis Foster

Florida faces many issues in HOA land, not the least of which is rising insurance rates. There’s also the issue of maintenance, with big structures like high-rise buildings (e.g. Surfside collapse) on many owners’ minds. Salty air has its consequences.

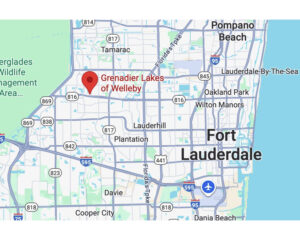

There’s now another developing story out of Fort Lauderdale regarding Grenadier Lakes at Welleby’s, a condominium complex of low-rise buildings that lost its board of directors when they all quit, but not before a large loan was taken out to cover maintenance for structural trouble, some of which was for repair of a seawall.

Except the HOA is well inland, located 22 miles from the coast. There is no seawall.

A newly elected 27-year-old board member commented on CBS News:

“We don’t have a seawall,” Keith Tannenbaum said. “In my opinion, it looks like somebody from this association walked into the bank and said I need $3 million, and the bank just said, ‘Here you go.'”

The bank that loaned the money is now demanding a $3 million assessment to residents.

The CBS story is a little confusing, but it seems that this all started when the HOA residents complained about roof leaks and mold. Increasing structural problems at the time had the community facing mandatory evacuation orders. So the board resigned. After a new board was elected, they hired engineers. Repair estimates for the condo structure came in at the range of $1.1-1.5 million. Then the bank called.

The association leaders said the bank wants collateral that the loan officer did not collect in 2022: a $3 million assessment demand. That assessment would not raise monthly payments for residents, association leaders said. However, anyone trying to sell their unit would have to pay their $17,000 share in full, association leaders said.

The property seems to have had problems dating back to at least 2022, when roof repairs were sorely needed and a construction loan was secured. Residents paid on the loan but the results of the fixes were decidedly mixed.

Crumbling concrete and a $3 million debt are causing a salty crisis in this HOA, and the bank wants an answer. According to the story:

The association board has until Friday to respond to the bank. If leaders refuse the demand, the bank could raise interest rates and push the community into bankruptcy.

You can check out the complete story from CBS HERE.

{kind=link}

{kind=link}

{kind=link}

{kind=link}